Form 497K Advisors’ Inner Circle

22 min readGet inside Wall Street with StreetInsider Premium. Claim your 1-week free trial here.

SUMMARY

PROSPECTUS

January

14, 2021

The

Advisors’ Inner Circle Fund III

First

Foundation Total Return Fund

(Class

A: FBBAX)

(Class

Y: FBBYX)

INVESTMENT

ADVISER:

BROOKMONT

CAPITAL MANAGEMENT, LLC

Before

you invest, you may want to review the Fund’s complete prospectus, which contains more information about the Fund and its

risks. You can find the Fund’s prospectus and other information about the Fund online at https://www.firstfoundationinc.com/first-foundation-funds.

You can also get this information at no cost by calling 800-838-0191, by sending an e-mail request to [email protected],

or by asking any financial intermediary that offers shares of the Fund. The Fund’s prospectus and statement of additional

information, both dated January 14, 2021, as they may be amended from time to time, are incorporated by reference into this summary

prospectus and may be obtained, free of charge, at the website, phone number or e-mail address noted above.

First

Foundation Total Return Fund

Investment

Objective

The

investment objective of the First Foundation Total Return Fund (the “Total Return Fund” or the “Fund”)

is to seek maximum total return (total return includes both income and capital appreciation).

Fund

Fees and Expenses

This

table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may be required to pay commissions

and/or other forms of compensation to a broker for transactions in Class Y shares, which are not reflected in the table or the

example below. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at

least $100,000 in Class A Shares of the Fund. More information about these and other discounts is available (i) from your financial

professional and (ii) in the “Purchasing, Selling and Exchanging Fund Shares – Purchasing Class A Shares” section

on page 49 of this prospectus. Investors investing in the Fund through an intermediary should consult Appendix A – Intermediary-Specific

Sales Charge Discounts and Waivers, which includes information regarding broker-defined sales charges and related discount and/or

waiver policies that apply to purchases through certain intermediaries.

Shareholder

Fees (fees paid directly from your investment)

|

|

Class |

Class |

|

Maximum |

5.75% |

None |

|

Maximum |

None1 |

None |

Annual

Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

|

Class |

Class |

|

Management |

0.50% |

0.50% |

|

Distribution |

0.25% |

None |

|

Other |

0.31% |

0.31% |

|

Acquired |

0.13% |

0.13% |

|

Total |

1.19% |

0.94% |

|

1 |

Class |

|

2 |

Other |

1

Example

This

Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds.

The

Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end

of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating

expenses (including capped expenses for the period described in the footnote to the fee table) remain the same. Although your

actual costs may be higher or lower, based on these assumptions your costs would be:

|

|

1 |

3 |

5 |

10 |

|

Class |

$689 |

$931 |

$1,192 |

$1,935 |

|

Class |

$96 |

$300 |

$520 |

$1,155 |

Portfolio

Turnover

The

Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio).

A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held

in a taxable account. These costs, which are not reflected in total annual Fund operating expenses or in the example, affect the

Fund’s performance. During its most recent fiscal year ended September 30, 2020, the portfolio turnover rate of the Highland

Total Return Fund (the “Predecessor Total Return Fund”), the Fund’s predecessor fund, was 73% of the average

value of its portfolio.

Principal

Investment Strategies

The

Fund seeks to achieve its investment objective by investing primarily in a combination of U.S. and foreign (non-U.S.) equity and

debt securities and cash. The Fund’s asset allocation process utilizes information from the Fund’s sub-adviser, First

Foundation Advisors (“FFA” or the “Sub-Adviser”), to diversify holdings across these asset classes and

to adjust the asset class weightings based on market and economic conditions. The Fund may also use various types of derivatives

(such as options, futures and options on futures) to gain exposure to certain types of securities as an alternative to investing

directly in such securities, to manage currency exposure and interest rate exposure (also known as duration), and to manage exposure

to credit quality. The Fund may hedge a portion of its foreign currency risk but is not required to do so.

2

The

Adviser has allocated all the assets of the Fund to be managed/advised by FFA. The Fund invests in equity securities, such as

common and preferred stocks, principally for their capital appreciation potential and investment-grade debt securities principally

for their income potential. The Fund invests in cash principally for the preservation of capital, income potential or maintenance

of liquidity. Within each asset class, the portfolio managers primarily use active security selection to choose securities based

on the perceived merits of individual issuers, although portfolio managers of different asset classes or strategies may place

different emphasis on the various characteristics of a company (as identified below) during the selection process. If the portfolio

managers believe market conditions provide for attractive valuations relative to more liquid investments, the Fund may also invest

in or hold illiquid or restricted securities. The Fund may focus in a particular sector or sectors of the economy, the risks of

which are disclosed in the Principal Risks section below.

The

Fund may pursue a “growth style” of investing, meaning that the Fund may invest in equity securities of companies

that the Adviser believes will increase their earnings at a certain rate that is generally higher than the rate expected for non-growth

companies. The Fund may also engage in value investing. Value investing focuses on companies with stocks that appear undervalued

in light of factors such as the company’s earnings, book value, revenues or cash flow.

The

portfolio managers seek to identify equity securities of companies with characteristics such as:

|

● |

strong |

|

● |

favorable |

|

● |

a |

|

● |

high |

|

● |

large |

The

portfolio managers seek to identify debt securities with characteristics such as:

|

● |

attractive |

|

● |

the |

3

|

● |

reasonable |

The

portfolio managers may consider selling a security when one of these characteristics no longer applies, or when valuation becomes

excessive and more attractive alternatives are identified.

The

portion of the Fund invested in debt securities normally has a weighted average maturity of approximately five to ten years, but

is subject to no limitation with respect to the maturities of the instruments in which it may invest.

The

Fund may also invest to a lesser extent in high yield securities (also known as “junk securities”), equity and debt

securities of companies that are located in emerging market countries, and exchange-traded funds (“ETFs”) and closed-end

funds to gain exposure to securities, including those of U.S. issuers that are principally engaged in or related to the real estate

industry and to securities in emerging markets. The Fund may also invest in real estate investment trusts (“REITs”).

As

of the date of this Prospectus, the Fund has significant exposure to companies that operate in the Communications Sector and Real

Estate sector.

Principal

Risks

As

with all mutual funds, there is no guarantee that the Fund will achieve its investment objective. You could lose money by investing

in the Fund. A Fund share is not a bank deposit and is not insured or guaranteed by the FDIC or any government agency. The

principal risk factors affecting shareholders’ investments in the Fund are set forth below.

Market

Risk — The risk that the market value of a security may move up and down, sometimes rapidly and unpredictably. Market

risk may affect a single issuer, an industry, a sector or the equity market as a whole. In addition, the impact of any epidemic,

pandemic or natural disaster, or widespread fear that such events may occur, could negatively affect the global economy, as well

as the economies of individual countries, the financial performance of individual companies and sectors, and the markets in general

in significant and unforeseen ways. Any such impact could adversely affect the prices and liquidity of the securities and other

instruments in which the Fund invests, which in turn could negatively impact the Fund’s performance and cause losses on

your investment in the Fund.

4

Asset

Allocation Risk — The Fund is subject to asset allocation risk, which is the risk that the Sub-Adviser’s allocation

of the Fund’s assets among strategies will cause the Fund to underperform other funds with a similar investment objective

and/or underperform the markets in which the Fund invests.

Liquidity

Risk — The risk that certain securities may be difficult or impossible to sell at the time and price that the Fund would

like. The Fund may have to lower the price of the security, sell other securities instead or forego an investment opportunity,

any of which could have a negative effect on Fund management or performance. Liquidity risk may be heightened in the emerging

market countries in which the Fund invests, as a result of their markets being less developed.

Equity

Risk — Since it purchases equity securities, the Fund is subject to the risk that stock prices will fall over short

or extended periods of time. Historically, the equity markets have moved in cycles, and the value of the Fund’s equity securities

may fluctuate drastically from day to day. Individual companies may report poor results or be negatively affected by industry

and/or economic trends and developments. The prices of securities issued by such companies may suffer a decline in response. These

factors contribute to price volatility.

Large

Shareholder Risk — The risk that a significant percentage of the Fund’s shares may be owned or controlled by a

large shareholder, such as other funds or accounts, including those of which the Adviser, the Sub-Adviser or an affiliate of the

Adviser or Sub-Adviser, may have investment discretion. Accordingly, the Fund can be subject to the potential for large scale

inflows and outflows as a result of purchases and redemptions made by significant shareholders. These inflows and outflows could

be significant, could cause the Fund to sell securities at inopportune times in order to meet redemption requests, and could cause

the Fund’s portfolio turnover rate and transaction costs to rise, which may negatively affect the Fund’s performance

and have adverse tax consequences for Fund shareholders.

Real

Estate Sector Risk — Securities of companies principally engaged in the real estate sector may be subject to the risks

associated with the direct ownership of real estate. Risks commonly associated with the direct ownership of real estate include

(i) changes in general economic and market conditions; (ii) changes in the value of real estate properties; (iii) risks related

to local economic conditions, overbuilding and increased competition; (iv) increases in property taxes and operating expenses;

(v) changes in zoning laws; (vi) casualty and condemnation losses; (vii) variations in rental income, neighborhood values or the

appeal of property to tenants; (viii) the availability of financing; and (ix) changes in interest rates and quality of credit

extended.

5

Value

Style Risk — If the Adviser’s assessment of market conditions, or a company’s value or prospects for exceeding

earnings expectations is wrong, the Fund could suffer losses or produce poor performance relative to other funds. In addition,

“value stocks” can continue to be undervalued by the market for long periods of time.

Communications

Sector Risk — Communications Sector Risk is the risk that the securities of, or financial instruments tied to the performance

of, issuers in the Communications Sector that the Fund purchases will underperform the market as a whole. To the extent that the

Fund’s investments are exposed to issuers conducting business in the Communications Sector (“Communications Companies”),

the Fund is subject to legislative or regulatory changes, adverse market conditions and/or increased competition affecting the

Communications Sector. The prices of the securities of Communications Companies may fluctuate widely due to both federal and state

regulations governing rates of return and services that may be offered, fierce competition for market share, and competitive challenges

in the U.S. from foreign competitors engaged in strategic joint ventures with U.S. companies, and in foreign markets from both

U.S. and foreign competitors. In addition, recent industry consolidation trends may lead to increased regulation of Communications

Companies in their primary markets.

Counterparty

Risk — There is a risk that the Fund may incur a loss arising from the failure of another party to a contract (the counterparty)

to meet its obligations. Substantial losses can be incurred if a counterparty fails to deliver on its contractual obligations.

Credit

Risk — The risk that the issuer of a security or the counterparty to a contract will default or otherwise become unable

to honor a financial obligation.

Currency

Risk — As a result of the Fund’s investments in securities or other investments denominated in, and/or receiving

revenues in, foreign currencies, the Fund will be subject to currency risk. Currency risk is the risk that foreign currencies

will decline in value relative to the U.S. dollar or, in the case of hedging positions, that the U.S. dollar will decline in value

relative to the currency hedged. In either event, the dollar value of an investment in the Fund would be adversely affected. Currency

exchange rates may fluctuate in response to, among other things, changes in interest rates, intervention (or failure to intervene)

by U.S. or foreign governments, central banks or supranational entities, or by the imposition of currency controls or other political

developments in the United States or abroad.

6

Fixed

Income Market Risk — The prices of the Fund’s fixed income securities respond to economic developments, particularly

interest rate changes, as well as to perceptions about the creditworthiness of individual issuers, including governments and their

agencies. Generally, the Fund’s fixed income securities will decrease in value if interest rates rise and vice versa. In

a low interest rate environment, risks associated with rising rates are heightened. Declines in dealer market-making capacity

as a result of structural or regulatory changes could decrease liquidity and/or increase volatility in the fixed income markets.

In the case of foreign securities, price fluctuations will reflect international economic and political events, as well as changes

in currency valuations relative to the U.S. dollar. In response to these events, the Fund’s value may fluctuate and/or the

Fund may experience increased redemptions from shareholders, which may impact the Fund’s liquidity or force the Fund to

sell securities into a declining or illiquid market.

Derivatives

Risk — The Fund’s use of futures contracts and options is subject to market risk, leverage risk, correlation risk

and liquidity risk. Leverage risk, liquidity risk and market risk are described elsewhere in this section. Correlation risk is

the risk that changes in the value of the derivative may not correlate perfectly with the underlying asset, rate or index. Each

of these risks could cause the Fund to lose more than the principal amount invested in a derivative instrument. Some derivatives

have the potential for unlimited loss, regardless of the size of the Fund’s initial investment. The Fund’s use of

derivatives may also increase the amount of taxes payable by shareholders. Both U.S. and non-U.S. regulators are in the process

of adopting and implementing regulations governing derivatives markets, the ultimate impact of which remains unclear.

Foreign

Investment/ Emerging Markets Risk — The risk that non-U.S. securities may be subject to additional risks due to, among

other things, political, social and economic developments abroad, currency movements and different legal, regulatory and tax environments.

These additional risks may be heightened with respect to emerging market countries because political turmoil and rapid changes

in economic conditions are more likely to occur in these countries.

7

Investments

in Investment Company Risk — When the Fund invests in an investment company, including closed-end funds and ETFs, in

addition to directly bearing the expenses associated with its own operations, it will bear a pro rata portion of the investment

company’s expenses. Further, while the risks of owning shares of an investment company generally reflect the risks of owning

the underlying investments of the investment company, the Fund may be subject to additional or different risks than if the Fund

had invested directly in the underlying investments. For example, the lack of liquidity in an ETF could result in its share price

being more volatile than that of the underlying portfolio securities. Certain closed-end investment companies issue a fixed number

of shares that trade on a stock exchange at a premium or a discount to their net asset value (“NAV”). As a result,

a closed-end fund’s share price fluctuates based on what another investor is willing to pay rather than on the market value

of the securities in the fund.

Growth

Style Risk — If a growth company does not meet the Adviser’s expectations that its earnings will increase at a

certain rate, the price of its stock may decline significantly, even if it has increased earnings. Many growth companies do not

pay dividends. Companies that do not pay dividends often have greater stock price declines during market downturns. Over time,

a growth investing style may go in and out of favor, and when out of favor, may cause the Fund to underperform other funds that

use differing investing styles.

Hedging

Risk — Hedging risk is the risk that instruments used for hedging purposes may also limit any potential gain that may

result from the increase in value of the hedged asset. To the extent that the Fund engages in hedging strategies, there can be

no assurance that such strategy will be effective or that there will be a hedge in place at any given time.

Below

Investment Grade Securities (Junk Bonds) Risk — Fixed income securities rated below investment grade (junk bonds) involve

greater risks of default or downgrade and are generally more volatile than investment grade securities because the prospect for

repayment of principal and interest of many of these securities is speculative. Because these securities typically offer a higher

rate of return to compensate investors for these risks, they are sometimes referred to as “high yield bonds,” but

there is no guarantee that an investment in these securities will result in a high rate of return.

8

Interest

Rate Risk — The risk that a rise in interest rates will cause a fall in the value of fixed income securities, including

U.S. Government securities, in which the Fund invests. Although U.S. Government securities are considered to be among the safest

investments, they are not guaranteed against price movements due to changing interest rates. A low interest rate environment may

present greater interest rate risk because there may be a greater likelihood of rates increasing and rates may increase more rapidly.

Interest rate risk may be heightened for investments in emerging market countries.

Large

Capitalization Company Risk — The risk that larger, more established companies may be unable to respond quickly to new

competitive challenges such as changes in technology and consumer tastes. Larger companies also may not be able to attain the

high growth rates of successful smaller companies.

Small-

and Mid-Capitalization Company Risk — The small- and mid-capitalization companies in which the Fund may invest may be

more vulnerable to adverse business or economic events than larger, more established companies. In particular, investments in

these small- and mid-sized companies may pose additional risks, including liquidity risk, because these companies tend to have

limited product lines, markets and financial resources, and may depend upon a relatively small management group. Therefore, small-

and mid-cap stocks may be more volatile than those of larger companies. These securities may be traded over-the-counter or listed

on an exchange.

Micro-Capitalization

Company Risk — Micro-capitalization companies may be newly formed or in the early stages of development with limited

product lines, markets or financial resources. Therefore, micro-capitalization companies may be less financially secure than large-,

mid- and small-capitalization companies and may be more vulnerable to key personnel losses due to reliance on a smaller number

of management personnel. In addition, there may be less public information available about these companies. Micro-cap stock prices

may be more volatile than large-, mid- and small-capitalization companies and such stocks may be more thinly traded and thus difficult

for the Fund to buy and sell in the market.

9

Mortgage-Backed

Securities Risk — Mortgage-backed securities are affected significantly by the rate of prepayments and modifications

of the mortgage loans backing those securities, as well as by other factors such as borrower defaults, delinquencies, realized

or liquidation losses and other shortfalls. Mortgage-backed securities are particularly sensitive to prepayment risk, which is

described below, given that the term to maturity for mortgage loans is generally substantially longer than the expected lives

of those securities; however, the timing and amount of prepayments cannot be accurately predicted. The timing of changes in the

rate of prepayments of the mortgage loans may significantly affect the Fund’s actual yield to maturity on any mortgage-backed

securities, even if the average rate of principal payments is consistent with the Fund’s expectation. Along with prepayment

risk, mortgage-backed securities are significantly affected by interest rate risk, which is described above. In a low interest

rate environment, mortgage loan prepayments would generally be expected to increase due to factors such as refinancings and loan

modifications at lower interest rates. In contrast, if prevailing interest rates rise, prepayments of mortgage loans would generally

be expected to decline and therefore extend the weighted average lives of mortgage-backed securities held or acquired by the Fund.

Cyber

Security Risk — The Fund and its service providers may be susceptible to operational and information security risks

resulting from a breach in cyber security, including cyber-attacks. Cyber-attacks may interfere with the processing of shareholder

transactions, impact the Fund’s ability to calculate its NAV, cause the release of private shareholder information or confidential

company information, impede redemptions, subject the Fund to regulatory fines or financial losses, and cause reputational damage.

Similar types of cyber security risks are also present for issuers of securities in which the Fund invests.

Prepayment

Risk — The risk that, in a declining interest rate environment, fixed income securities with stated interest rates may

have the principal paid earlier than expected, requiring the Fund to invest the proceeds at generally lower interest rates.

Portfolio

Turnover Risk — Due to its investment strategy, the Fund may buy and sell securities frequently. This may result in

higher transaction costs and additional capital gains tax liabilities, which may affect the Fund’s performance.

10

REITs

Risk — REITs are pooled investment vehicles that own, and usually operate, income-producing real estate or finance real

estate. REITs are susceptible to the risks associated with direct ownership of real estate, as discussed elsewhere in this section.

REITs typically incur fees that are separate from those of the Fund. Accordingly, the Fund’s investments in REITs will result

in the layering of expenses such that shareholders will indirectly bear a proportionate share of the REITs’ operating expenses,

in addition to paying Fund expenses. REIT operating expenses are not reflected in the fee table and example in this prospectus.

Restricted

Securities Risk — Investments in restricted securities may be illiquid. Although these securities may be resold in privately

negotiated transactions, the prices realized from these sales could be less than those originally paid by the Fund or less than

what may be considered the fair value of such securities. Further, restricted securities may not be subject to the disclosure

and other investor protection requirements that might be applicable to unrestricted securities. In order to sell restricted securities,

the Fund may have to bear the expense of registering the securities for resale and the risk of substantial delays in effecting

the registration. Other transaction costs may be higher for restricted securities than unrestricted securities.

LIBOR

Replacement Risk — The elimination of the London Inter-Bank Offered Rate (“LIBOR”) may adversely affect

the interest rates on, and value of, certain Fund investments for which the value is tied to LIBOR. The U.K. Financial Conduct

Authority has announced that it intends to stop compelling or inducing banks to submit LIBOR rates after 2021. However, it remains

unclear if LIBOR will continue to exist in its current, or a modified, form. Alternatives to LIBOR are established or in development

in most major currencies, including the Secured Overnight Financing Rate (“SOFR”), which is intended to replace U.S.

dollar LIBOR. Markets are slowly developing in response to these new rates. Questions around liquidity impacted by these rates,

and how to appropriately adjust these rates at the time of transition, remain a concern for the Fund. Accordingly, it is difficult

to predict the full impact of the transition away from LIBOR on the Fund until new reference rates and fallbacks for both legacy

and new products, instruments and contracts are commercially accepted.

11

Performance

Information

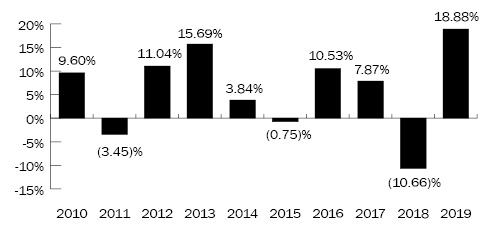

The

bar chart and the performance table below illustrate the risks and volatility of an investment in the Fund by showing changes

in the Fund’s Class A shares’ performance from year to year for the past 10 years and by showing how the Fund’s

Class A shares’ and Class Y shares’ average annual total returns for 1, 5 and 10 years compare with those of a broad

measure of market performance. The bar chart does not reflect the deduction of applicable sales charges for Class A shares. If

sales charges had been reflected, the returns for Class A shares would be less than those shown below. Of course, the Fund’s

past performance (before and after taxes) does not necessarily indicate how the Fund will perform in the future.

Before

the Fund commenced operations, the Fund acquired the assets and liabilities of the Predecessor Total Return Fund (the “Reorganization”).

After being approved by shareholders of the Predecessor Total Return Fund, the Reorganization occurred on January 11, 2021. As

a result of the Reorganization, the Fund assumed the performance and accounting history of the Predecessor Total Return Fund prior

to the date of the Reorganization. Accordingly, the performance shown for periods prior to the Reorganization represents the performance

of the Predecessor Total Return Fund. The Predecessor Total Return Fund’s returns in the bar chart and table have not been

adjusted to reflect the Fund’s expenses. If the Predecessor Total Return Fund’s performance information had been adjusted

to reflect the Fund’s expenses, the performance may have been higher or lower for a given period depending on the expenses

incurred by the Predecessor Total Return Fund for that period.

The

Predecessor Total Return Fund’s performance prior to February 1, 2015 reflects returns achieved when the Predecessor Total

Return Fund was sub-advised by a different sub-adviser. If the Predecessor Total Return Fund’s latter management had been

in place for periods prior to February 1, 2015, the performance information shown for such periods would have been different.

12

Updated

performance information is available by calling 800-838-0191 or by visiting the Fund’s website at https://www.firstfoundationinc.com/first-foundation-funds.

|

Best |

Worst |

|

8.98% |

(12.51)% |

|

(03/31/2019) |

(09/30/2011) |

Average

Annual Total Returns for Periods Ended December 31, 2019

This

table compares the Predecessor Total Return Fund’s average annual total returns for the periods ended December 31, 2019

to those of an appropriate broad based index.

After-tax

returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact

of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown.

After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k)

plans or individual retirement accounts. After-tax returns are shown for Class A shares only. After-tax returns for Class Y shares

will vary.

13

|

FIRST |

1 |

5 |

10 |

|

Fund |

|

|

|

|

Class |

12.03% |

3.45% |

5.28% |

|

Class |

19.19% |

4.92% |

6.15% |

|

Fund |

|

|

|

|

Class |

11.86% |

2.25% |

4.42% |

|

Fund |

|

|

|

|

Class |

7.24% |

2.34% |

3.99% |

|

S&P |

31.48% |

11.68% |

13.54% |

|

Bloomberg |

8.72% |

3.05% |

3.74% |

|

1 |

Class |

|

2 |

Class |

Investment

Advisers

Brookmont

Capital Management, LLC serves as investment adviser to the Fund. First Foundation Advisors serves as investment sub-adviser to

the Fund.

Portfolio

Managers

John

Hakopian, President of FFA, has managed the Fund since its inception in 2021 and managed the Predecessor Total Return Fund beginning

in 2015.

Jim

Garrison, Portfolio Manager, has managed the Fund since its inception in 2021 and managed the Predecessor Total Return Fund beginning

in 2015.

Eric

Speron, Portfolio Manager, has managed the Fund since its inception in 2021 and managed the Predecessor Total Return Fund beginning

in 2015.

14

Purchase

and Sale of Fund Shares

You

may generally purchase or redeem shares on any day that the New York Stock Exchange (“NYSE”) is open for business.

Purchase

minimum (for Class A shares) (reduced for certain accounts)

|

|

By |

By |

Automatic |

|||||||||

|

Initial |

$ | 500 | $ | 1,000 | $ | 25 | ||||||

|

Subsequent |

$ | 100 | $ | 1,000 | $ | 25 | ||||||

There

is no program asset size or minimum investment requirements for initial and subsequent purchases of shares by eligible omnibus

account investors.

Purchase

minimum (for Class Y Shares) (eligible investors only)

|

Initial |

None |

|

Subsequent |

None |

Class

Y Shares are available to investors who invest through programs or platforms maintained by an authorized financial intermediary.

Individual

investors that invest directly with the Fund are not eligible to invest in Class Y Shares.

The

Fund may accept investments of smaller amounts in its sole discretion.

If

you own your shares directly, you may redeem your shares by contacting the Fund directly by mail at: Brookmont Funds, PO Box 219009,

Kansas City, MO 64121 (Express Mail Address: Express Mail Address: Brookmont Funds, c/o DST Systems, Inc., 430 W 7th St, Kansas

City, MO 64105) or telephone at 800-838-0191.

If

you own your shares through an account with a broker or other financial intermediary, contact that broker or financial intermediary

to redeem your shares. Your broker or financial intermediary may charge a fee for its services in addition to the fees charged

by the Fund.

Tax

Information

The

Fund intends to make distributions that may be taxed as ordinary income or capital gains, unless you are investing through a tax-deferred

arrangement, such as a 401(k) plan or individual retirement account (“IRA”), in which case your distribution will

be taxed when withdrawn from the tax-deferred account.

15

Payments

to Broker-Dealers and Other Financial Intermediaries

If

you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related

companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest

by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask

your salesperson or visit your financial intermediary’s website for more information.

16