Northern summer months inventory industry lull sees…

5 min read

(Image: Adobe Inventory)

Equity sector volatility has declined down below its prolonged-term average and price shares are protecting their guide on advancement shares. Fund professionals stay good on the fairness outlook. But is this the tranquil in advance of the storm?

It is counterintuitive to believe that as worldwide growth prospects have looked far better and far better, worth shares have benefited much more than development shares. So much so that they have attained sufficient impetus to pull in advance of a universe that has been dominated by sharp rallies in Massive Five tech shares during the pandemic.

In the course of May, the MSCI Growth Index slipped .13%, while the MSCI Price Index obtained 3% in the course of the thirty day period. 12 months to date, the outperformance is even much more pronounced, with growth shares (up 6.5%) delivering much less than 50 percent the general performance of their price counterparts (16.7%).

These overall performance differentials again up investment decision views from previously this year that value was possible to overtake development soon after many years of underperformance. At the coronary heart of the change in relative effectiveness are the upbeat global development prospective buyers and the connected increase in inflation expectations.

There is some debate about how significantly macro aspects contribute to the general performance of stock markets. The latest investigate executed by Goldman Sachs Asset Administration located that even though financial growth could impact fairness performance, micro matters additional, with most effectiveness coming from stocks and not nations.

It notes that investors typically concern how their sights on economic advancement should really advise how they choose to spend in designed and emerging marketplaces.

“Economic theory implies that development influences fairness marketplaces in levels: 1) higher corporate profit growth, which prospects to 2) greater EPS growth, which last but not least interprets into 3) an boost in stock charges. Although this kind of a development can make intuitive feeling, in practice, we do not see a significantly solid statistical relationship.”

In accordance to historic data, there is some beneficial impact on fairness marketplace performance. Still, it is not to a substance extent, as the graph underneath displays, with the energy of the romantic relationship .3 as opposed to a excellent correlation of 1.

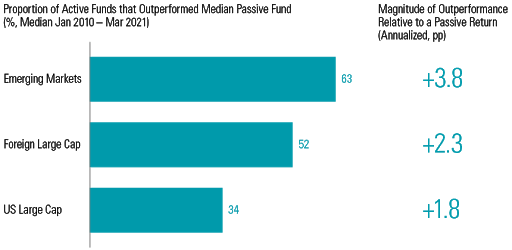

When it comes to inventory choice, Goldman Sachs points out that facts due to the fact 2010 present that “a major proportion” of international fund professionals have shipped returns in surplus of their passive counterparts via their lively stock assortment. As proven in the graph down below, Its analysis puts the outperformance of emerging marketplace and international substantial-cap administrators compared to the median passive fund at 3.8 proportion points and 2.3 share factors, respectively.

All over again on the lookout from a macro point of view, it would be challenging to attribute the outperformance of rising current market stock markets of late to their financial growth prospective buyers for the reason that they lag the state-of-the-art economies in an progressively bifurcated world wide economic restoration.

Even so, the MSCI Rising Marketplace Index shipped 2.3% in Might versus the MSCI World’s 1.2%. An increasing range of fund administrators have expressed a desire for very carefully selected rising markets alternatively than the shares detailed in sophisticated economies and buying and selling at a lot bigger valuations.

Nonetheless, there looks minimal indicator of a turnaround in the rise in made stock markets. Final 7 days world-wide equities achieved a new substantial, and the S&P 500 remains inside easy sight of its all-time significant. US stock markets have occur a little bit off the boil in May possibly and early June, with the S&P 500 .5% in advance just after the very first 7 days and the Nasdaq 1% following declining 1.2% in Could.

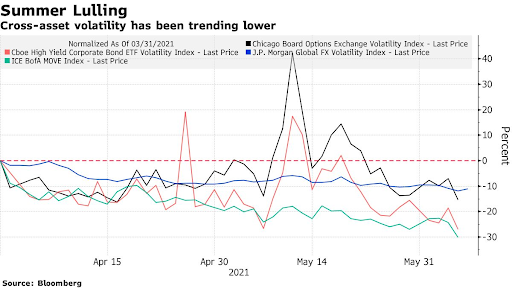

Equity industry volatility, as measured by the CBOE VIX, the so-called world-wide dread index, has also subsided to all around 16 when compared with the 37-as well as large reached in late January this year. According to Bloomberg, volatilities across other assets, including company bonds, authorities bonds and overseas trade, have been declining as well, as revealed in the graph under.

But before you get lulled into a wrong sense of complacency, bear in mind that the inflation debate is nowhere close to ending and, with eurozone inflation coming in at 2% this 7 days and the US CPI established to be produced in just the subsequent week, it may perhaps be the serene ahead of the storm.

Nevertheless, UBS main investment decision officer Mark Haefele is self-assured that the backdrop for stocks continues to be good, justified by the good financial backdrop, a solid earnings outlook, and ongoing plan assistance.

He places forward 3 arguments that help a continued rise in equities:

- Economic knowledge factors to accelerating progress, even though the uptick in inflation appears narrow and most likely to be short-lived.

- The recovery in global earnings is in full swing.

- Policymakers – equally fiscal and monetary – appear to be keen to permit economies operate incredibly hot.

His base line: “Economic data previous week ongoing to issue to soaring inflation amid larger power charges. But the increase should really establish narrow and short-lived. With expansion accelerating, we consider the financial outlook is benign for stocks and anticipate cyclical pieces of the sector to outperform.”

Capital Economics concurs, believing that buyers shouldn’t fret about inflation posing a danger to US shares. It claims that inflation will only be a problem for shares, “if it hurts the actual development outlook or potential customers to a sharp tightening of serious monetary policy” – one thing the economic consultancy does not expect to materialize before long. As these, it expects the S&P 500 to carry on rising about the subsequent number of decades, but notes that tech and growth shares “could lag broader sector gains”.

It is tricky to bank on any definitive sights on where by the economic system or economic markets are going when a lot of unknowns lie in advance. Even though arguments in favour of equities can be convincing, these optimistic Northern summer season stock sector sentiments may not prove lasting. When volatility re-emerges, as it will, it is likely to verify much wiser to be invested in a diversified portfolio throughout asset lessons and locations. DM/BM

![]()