Russia’s FX reserves slip from its grasp

7 min readThe Central Financial institution of Russia’s substantial reserves stockpile was meant to sustain the currency’s security in the face of current market stress.

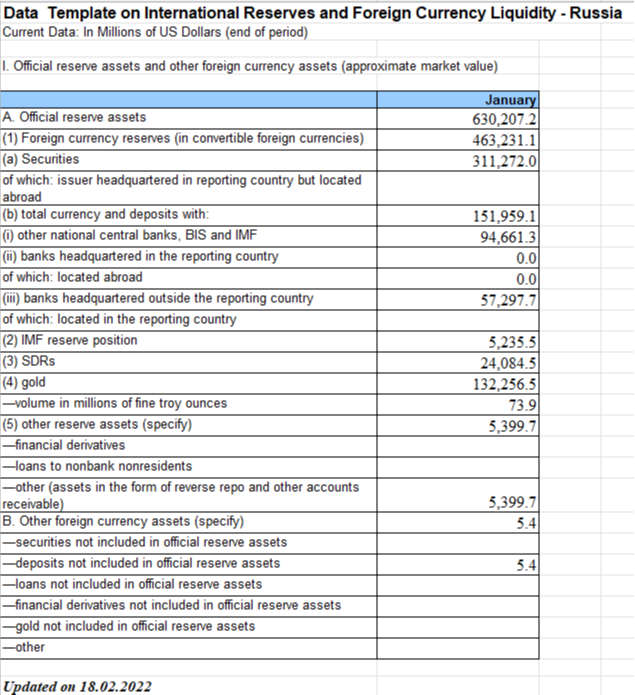

The reserves — worth $630bn, as of the close of January — are made up of property and deposits denominated in the world’s significant currencies (that is, the greenback, euro, sterling and the yuan). As perfectly as pretty much 2,300 tonnes of gold.

The stockpile was there so that the central lender could intervene in overseas trade markets, shoring up the rouble in the celebration of volatility. There’s a Jedi intellect-trick element to setting up up reserves way too — if markets know you’ve obtained a load of them, they’re considerably less possible to obstacle you to use them.

The sanctions imposed by the US, EU and United kingdom versus the central lender are very likely to render a lot, if not very all, of these reserves useless. To have an understanding of what the CBR is, and isn’t, very likely to have at its disposal when the banking institutions open tomorrow early morning, it is worthy of using a shut glimpse at what is recognized as the “Data Template for Global Reserves and Foreign Currency Liquidity”.

The snapshot under was taken from the Twitter account of previous Alphavillain Matthew Klein. We attempted to find the formal facts on the central bank’s web site, but it was no extended offered.

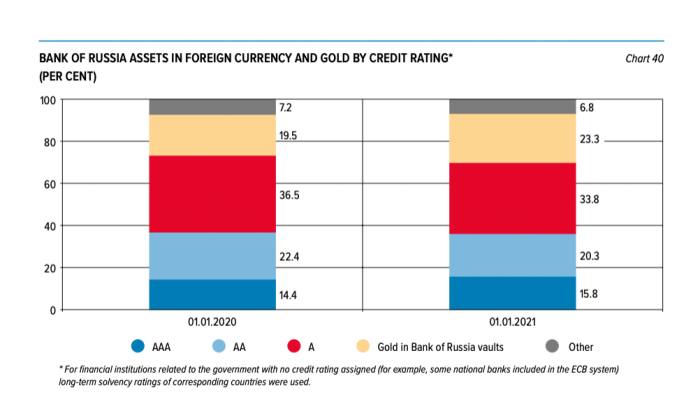

Securities make up a very little additional than half ($311bn) of what the CBR experienced at its disposal. According to its annual report, these assets had been largely hugely rated, with just 6.8 for each cent of them holding significantly less than an A rating.

Supplied their superior rankings, most of them will likely be hugely liquid and straightforward to offer in situations of panic. But how does the Russian central lender convert these securities into money in the function that it desires obtain to pounds or euros rapidly? Properly, it desires to depend on world-wide finance.

Here’s how Ousmène Mandeng, a browsing fellow at the London University of Economics and Political Science who has expended decades performing in the field of central lender reserve management, described it to us:

Overseas trade reserves are not held by central banking institutions. Securities and cash never ever move, every thing is external . . .

In the case of securities, central banking institutions would check with their brokers to provide the asset in question . . . In the case of, say, a German governing administration bond [that the CBR owns], the broker in Frankfurt will contact other brokers to announce the sale and, once a cost is agreed, will instruct the custodian of the stability to transfer it to the purchaser. On receipt of payment into a financial institution account, normally in Frankfurt, the custodian will instruct the central safety depository to assign the consumer as the new operator. The central bank’s then credited the proceeds at their account with the broker.

The proceeds could then be employed to instruct the broker, or overseas exchange sellers, most of whom are in London, to purchase the rouble at a unique level. The vendor will commonly be a Russian commercial bank. Seller and buyer may perhaps effectively share the similar correspondent lender. Once the buy is produced, the Bank of Russia would instruct its correspondent lender to credit history the seller’s account with euros.

Stopping the central bank employing its securities to stabilise the rouble would, consequently, include instructing the economic intermediaries that characteristic on this chain — brokers, custodians, central security depositories, foreign-trade sellers, and correspondent banking institutions — to freeze assets and cease acting on behalf of the central lender.

Judging by its modern conduct, there is substantially to advise the US will be prepared to do just that. In modern decades, Washington has generally furthered its overseas coverage through what’s referred to as the “weaponisation of finance”. What that has meant in observe is working with the dollar’s worldwide dominance to slash the financial authorities of Iran, Venezuela, and (most not long ago and extremely controversially) Afghanistan off from accessibility to their personal reserves.

There is a paradox at participate in here, concerning what the US is eager to do to its political enemies and the guidelines for the personal sector. Sovereign immunity usually protects a foreign central bank’s assets, typically held at the New York Fed, if they are “held for its very own account.” That balm has, nevertheless, been tested over the a long time in different US lawsuits in opposition to defaulting governments, as bondholders spied wealthy pickings in their overseas-exchange reserves. Nevertheless none of individuals lawsuits has long gone as significantly as the US government’s evermore frequent focusing on of the central financial institutions of its enemies.

In concentrating on central banking institutions, the authorities have invoked counter-terrorist and human rights legislation, alongside the US International Unexpected emergency Economic Powers Act. The latter in unique has established a powerful measure.

The most immediate way to sanction the CBR will be to place it on the so-termed Specifically Selected Nationals list, which despite its title includes establishments not just folks. This would bar US entities from working with them. When it will come to greenback obtain, that would place to a halt to each step of the system outlined by Mandeng.

The next chunk of reserves the CBR retains are in the sort of forex and deposits. These are well worth $152bn. Of this $152bn, about two-thirds is held in official institutions. That contains other central financial institutions, the Bank for Intercontinental Settlements and the IMF.

Central banking companies in the Eurosystem, wherever about a quarter of the CBR’s belongings are held, have now frozen the central bank’s accounts. The European Central Lender has stated it will put into practice all sanctions resolved by the EU and European governments. Joachim Nagel, the Bundesbank’s president, claimed earlier today that he “welcomes the actuality that detailed monetary sanctions have now been imposed and has campaigned for them.”

The BIS explained: “[Our] plan is that the institution does not acknowledge or go over banking associations. The BIS will adhere to sanctions, as relevant.”

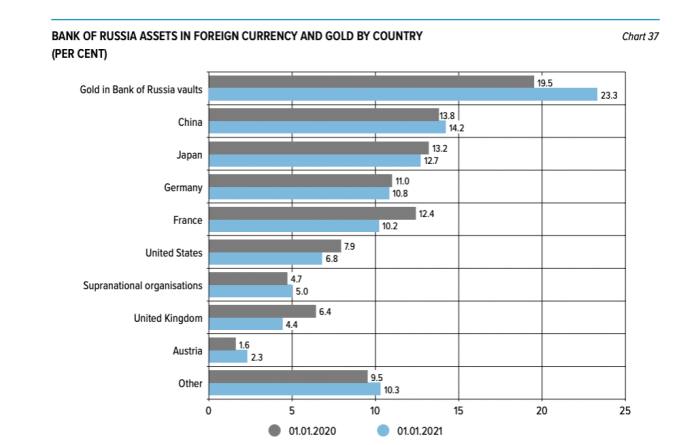

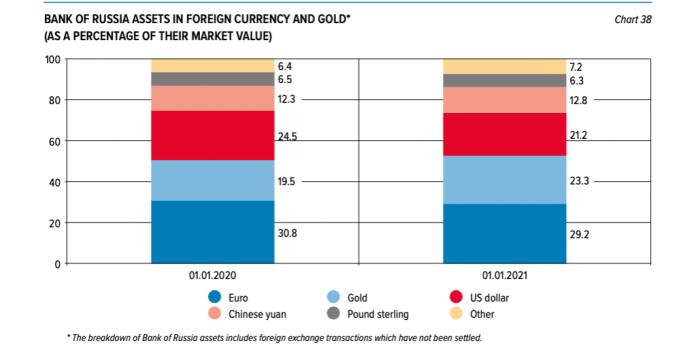

It is unclear how other authorities will behave. Notably China. In accordance to the CBR’s yearly report, as of the start of 2021, 14 for each cent of overseas trade reserves have been held in China — the most important share for any one particular condition. Nearly 13 for every cent of the reserves are in yuan or belongings denominated in yuan.

Mandeng states that China may perhaps give a implies for Russia to keep on investing with at least some pieces the world:

Russia may take payments for its exports in renminbi and maximize imports compensated in renminbi from China and potentially other international locations accepting renminbi. As renminbi-dependent payments will most probably be done by institutions outside the fast impact sphere of the West, this would function.

The other third of the CBR’s deposits are held at personal financial institutions. Once again, it is extremely hard to say what share of this $57bn is held in the US, United kingdom or EU. But as almost 60 per cent of the CBR’s reserves are in either dollars, euro or sterling, it’s honest to guess that it is additional than 50 percent.

Economic intermediaries in the rest of the planet may perhaps also not want to deal with the CBR, even if they are not specifically included by the sanctions. When the US puts you on its blacklist, it can have a chilling effect. Famously, Carrie Lam, Hong Kong’s chief, resorted to “piles of cash” soon after neighborhood establishments have been hesitant to bank her and other city officials who came less than US sanctions.

And then there is gold, the historic favourite of central financial institutions throughout the world. Like Russia’s monetary guardian. The CBR’s holdings are huge — the fifth most significant in the planet — and, in accordance to market trade overall body the Planet Gold Council, they’ve been amid the most significant purchasers of late. According to its yearly report, the entirety of the $130bn-truly worth of bullion is all stored in vaults in just the Russian Federation.

Holding all your gold this near to home is abnormal. Most of the world’s central banks hold a substantial portion in vaults beneath the Bank of England’s headquarters in Threadneedle Road, or shut to Wall Road, in the coffers of the New York Federal Reserve. The purpose getting that the City of London and New York are the twin centres of the world-wide gold sector, producing it much easier to purchase and offer bars.

Holding the gold in Russia, and not in London or New York, will make it more hard for the central bank to dispose of it in huge portions. At the exact same time, acquiring it near to property helps make it extremely challenging for the US, British isles and EU to properly impose sanctions on Russia’s bullion. Monetary pariah it could possibly be, but people who know the industry believe that it would be silly to suppose that Russia will be entirely frozen out. The entice of gold has been an ever-present all through record — specially in durations of geopolitical uncertainty. If Russia is advertising below industry premiums, then we believe anyone, somewhere will be willing to just take the risk.

We’re not going to spend also a lot attention to what else the CBR may perhaps, or may well not, have at its disposal arrive the early morning. SDRs or a number of billions in banknotes are not going to halt a currency’s collapse.

Feel otherwise? Thoughts in the standard position. Together with any guesses on where the rouble will close the day tomorrow.